Electric vehicle (EV) insurance that addresses batteries, charging equipment, repairs, and liability refers to policy language and optional endorsements that specifically consider the unique components and failure modes of electric drivetrains and associated hardware. Rather than treating an EV identically to an internal combustion vehicle, this coverage concept examines how battery packs, on-board charging systems, portable and fixed chargers, and specialized repair procedures are included, excluded, or limited under standard auto and property policies. The focus is on which events trigger coverage, how value and depreciation of battery capacity are treated, and whether repair networks and diagnostic processes are recognised by insurers.

Coverage distinctions often arise because battery packs and charging equipment can have higher replacement costs, different wear patterns, and manufacturer warranties that interact with insurance claims. Insurers may offer endorsements for battery failure due to sudden damage, for charging equipment loss or damage at home, or for specialized repair procedures performed by certified technicians. Liability considerations—such as third-party bodily injury and property damage arising from EV operation or charging incidents—remain part of comprehensive policy design but may have component-specific documentation and evidence requirements.

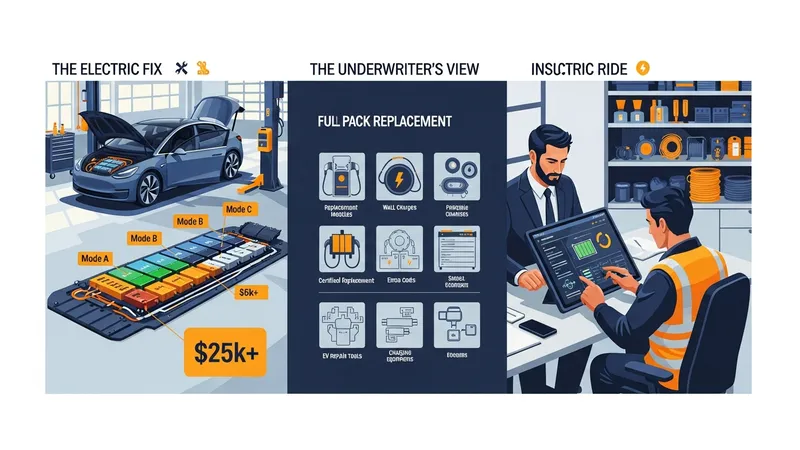

Battery-specific endorsements often define covered causes and exclusions. For example, coverage may apply where a battery experiences sudden physical damage from a collision or fire, whereas gradual capacity loss due to normal degradation is typically outside insurance and within manufacturer warranty or maintenance expectations. Policies that reference batteries can also state whether the insurer will cover replacement with a new, refurbished, or remanufactured component, and how depreciation is calculated. These clauses may interact with salvage rights, subrogation, and any transferable manufacturer warranty the vehicle retains.

Charging equipment coverage can be split between property and vehicle contexts. Home chargers and fixed EVSE may be eligible under a homeowner policy for incidents like theft or vandalism, while a vehicle-related endorsement might cover portable charging units that are lost or damaged while transported with the vehicle. Insurers may require documentation—such as purchase receipts, installation invoices, or serial numbers—to evaluate a claim. Electrical faults, improper installation, or third-party maintenance can be factors that affect whether a claim is accepted.

Repair and diagnostic coverage addresses both parts and labour. Modern EV repair can require manufacturer diagnostic access, calibrated tools, and trained technicians; insurers often account for these factors when estimating repair timelines and costs. Where OEM parts are specified, claims may reflect higher part costs and longer wait times. In some cases, policies may include guidelines about authorised repair facilities or may reimburse higher repair costs if evidence shows the technician met manufacturer training standards.

Liability and supporting policy features remain central to comprehensive EV insurance. Third-party bodily injury and property damage coverages function similarly to conventional policies, but certain EV-specific incidents—such as a fire originating in an onboard charger or a charging cable causing a property loss—may need additional documentation or be handled through property rather than auto provisions. Optional features like rental reimbursement or roadside assistance may have EV-specific limitations, such as restrictions on towing to qualified EV repair centres or on battery jump-start procedures.

In summary, assessing insurance for electric vehicles involves reviewing specific endorsements and policy language that address battery events, charger equipment, and repair protocols alongside standard liability elements. Understanding how sudden damage versus gradual degradation is treated, how charging equipment is classified between property and vehicle coverage, and how repair authorisation is handled can clarify likely outcomes in a claim. The next sections examine practical components and considerations in more detail.

Policies that address batteries and charging equipment commonly separate coverable events from routine maintenance and manufacturer warranty issues. Battery replacement due to collision, documented thermal events, or other sudden physical damage may be presented under collision or comprehensive triggers, while gradual capacity decline is often a warranty matter. Charging equipment may be covered under a homeowner policy for fixed domestic units or under vehicle-related endorsements for portable units. When assessing policy components, it can be useful to note whether the insurer specifies new-for-old replacement, depreciation schedules, or limits per component, and whether serial numbers or purchase records are required to validate a claim.

Some insurers define a battery’s insurable value in policy terms, which can influence payout methods: replacement cost, agreed value, or actual cash value after depreciation. Repair network language may appear in the same section, specifying authorised repairers or OEM part requirements. Charging equipment clauses sometimes include electrical fault exclusions or require proof of professional installation, and they may refer to third-party liability if a charging unit causes property damage. These technical distinctions typically influence claim acceptance and the settlement amount.

When both auto and homeowner policies could apply—such as with a garage‑mounted charger—there may be overlap or gaps. Coordination of benefits is an informational consideration: insurers may seek to determine primary and secondary sources of recovery, including manufacturer warranties or contractor liability where improper installation contributed. Policyholders may encounter requests for maintenance records, charger firmware logs, or photographic evidence describing condition before loss to support coverage under these components.

Insurers may also include sublimits specifically for non-standard vehicle equipment like portable charging units or home EVSE. These sublimits can affect how much is payable for repair or replacement and whether additional endorsements are available to raise limits. As EV adoption increases, some policies are adjusting language to explicitly reference EV components; readers may find it informative to compare clause phrasing across insurers to understand typical inclusions and exclusions without assuming uniform treatment.

Claim handling for EV components often requires more detailed documentation than standard auto claims due to diagnostic complexity and high‑value parts. Insurers may request diagnostic reports from certified repair shops, battery state‑of‑health (SoH) metrics, purchase invoices for chargers, and installation certificates for home units. When a battery exhibits signs of internal failure, a diagnostic log recorded by the vehicle’s control unit can be central evidence. Documentation that links the loss to a covered peril—such as collision, fire, or theft—typically forms the basis of an accepted claim, while absence of evidence may lead to investigatory follow-up or denial.

>

Insurers may require claimants to allow examination of the component, including sending a battery module to a lab for analysis, or permitting an on-site inspection of charging equipment. For incidents involving third parties—such as a contractor who installed the home charger—insurers may pursue subrogation and request contact details for those parties. Timeframes for submitting evidence and cooperating with a claim process are often set out in policy terms. Understanding typical document requests can help set expectations for processing times and potential outcomes.

Repair authorization procedures can be more involved when software or firmware data needs preservation for investigation. Some insurers prefer or mandate repair at authorised facilities with access to OEM diagnostic tools; others accept independent shops if they can provide certified diagnostics. The claim process may include assessment of whether a repair or replacement aligns with safety standards and manufacturer guidance, particularly where battery integrity and thermal management are concerned. These procedural steps often influence out-of-pocket exposure and settlement timelines.

When charging equipment is damaged, insurers may determine whether the loss is covered under property or vehicle provisions; this determination typically guides which documentation is needed. Proof of ownership, serial numbers, photos showing installation, and electrician receipts are commonly requested. Where policies overlap, communication between involved insurers and clear documentation usually determines coverage allocation. These procedural realities are intended to reduce ambiguity in settlement but may add administrative steps for claimants.

Pricing for EV insurance components can be influenced by several cost drivers that insurers commonly evaluate. Battery replacement or repair costs are a primary factor because battery modules can represent a substantial portion of vehicle value; replacement may range from several thousand to multiple tens of thousands of currency units depending on vehicle size and chemistry. Repair complexity, availability of parts, and geographic labor rates can all affect pricing. Charging equipment replacement costs are typically lower but vary widely by charger type, installation complexity, and whether electrical work is required.

Underwriting for EVs may account for vehicle value, battery capacity, historical reliability of a specific model, and kilometres typically driven; these variables commonly influence premiums. Insurers sometimes adjust rates where repair networks are limited, because towing and transport to authorised facilities add expense. Optional coverages such as specialised roadside assistance for EVs or higher limits for non-standard equipment can increase premium if selected. Pricing models may also evolve as collective claims experience with EV batteries and charging infrastructure becomes more robust.

Loss frequency and severity data for EVs are still maturing in many markets, which can result in cautious pricing patterns. Where insurers lack extensive claims history for particular models, they may rely on conservative estimates and reinsurance costs when setting rates. External factors—such as battery material prices, supply chain constraints for replacement modules, and changes in repair technologies—can also influence long‑term premium trends. These market-level considerations are typically reflected in policy filings and rate setting over time.

Deductible structure is another consideration that affects cost exposure in the event of a claim. Higher deductibles can lower premiums but increase out-of-pocket expense if a battery or charging unit requires claim-related replacement. Some insurers may offer per-component deductibles or limits for non-standard equipment, which alters the economics of filing a claim. Policyholders and analysts often weigh these patterns when comparing coverages, keeping in mind that specific financial outcomes depend on individual policy terms and local pricing environments.

Ownership-related risks for EVs include battery degradation, charging behaviour, storage conditions, and exposure to environmental hazards. Frequent fast-charging or exposure to high ambient temperatures can affect battery life over time, which insurers may view as contributing factors when assessing liability for battery failures. Policies may include language on permitted use, and some underwriters consider owner behaviours—such as use in ride‑hailing or commercial delivery—when evaluating risk classification and applicable premium. These distinctions can influence available options for coverage and underwriting outcomes.

Policy feature considerations relevant to EV owners include replacement cost versus depreciated value settlements, defined limits for non-standard equipment, roadside assistance tailored to EV needs, and whether rental reimbursement covers similarly equipped replacement vehicles. Owners may encounter policies that specify authorised repair facilities or require pre-approval for certain repairs; such features can affect turnaround times for repairs and clarity on who pays for diagnostic procedures. These features are often framed as options rather than requirements in policy documents.

Record keeping and preventive documentation are practical considerations insurers may view favourably when processing claims. Maintaining purchase receipts for charging equipment, installation certificates, manufacturer warranty details, and maintenance logs for the vehicle can support a claim by establishing provenance and condition prior to loss. While documentation does not guarantee coverage, it typically reduces administrative friction and helps clarify whether a loss falls within a policy’s covered perils or is subject to an exclusion.

Finally, evolving regulatory frameworks and industry standards around EV safety and charging infrastructure can affect coverage boundaries over time. As testing protocols, repair certifications, and interoperability standards become more widespread, insurers may update policy language to reflect prevailing norms. Monitoring such developments can provide insight into how coverage for batteries, charging equipment, and associated repairs is likely to be described in future policy forms without implying that any single approach is universally applicable.