When evaluating care at a privately run hospital, it is useful to separate three interrelated areas: how fees are established, how bills are itemized and presented, and how third‑party payers such as insurers respond. Fees at private facilities often reflect a combination of facility charges (use of rooms, operating theatres, equipment), professional fees (physicians, anaesthetists), and ancillary charges (medicines, imaging, laboratory tests). Billing structures determine whether those components appear as separate line items, bundled packages, or negotiated rates under contract. Understanding these components in neutral terms can help patients and advisors interpret invoices and compare likely outlays across providers.

Billing practices in private hospitals may vary by contract type, service line, and regional norms. Some hospitals publish package rates for common procedures, while others bill strictly by individual service codes. Insurance arrangements add an additional layer: plans may cover a portion of facility charges, require preauthorization for specific services, or apply case-based payments. Billing cycles, timing of claims submissions, and whether the provider accepts an insurer’s network rate can all influence the final patient balance. These factors combine to create a landscape where transparency and documentation are central to evaluating potential costs.

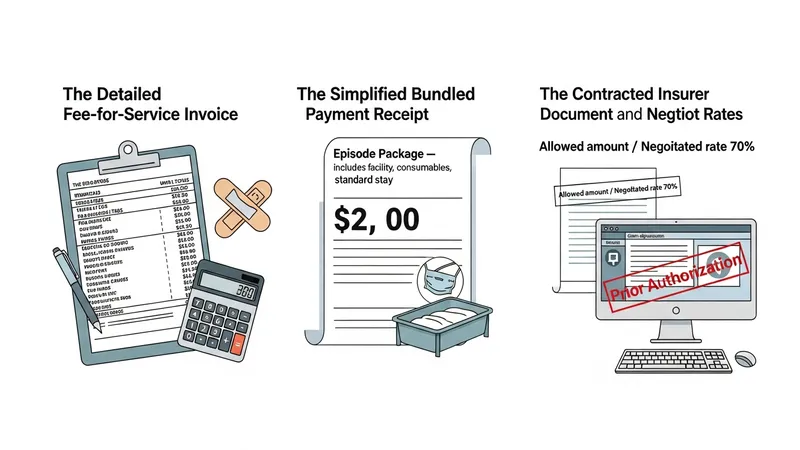

Fee-for-service models may provide detailed invoices but can also lead to variability in total charges depending on tests ordered and length of stay. Bundle pricing can simplify estimate comparisons but sometimes omits specific high-cost elements such as implants or prolonged intensive care. When hospitals operate under negotiated insurer rates, patients typically see the insurer’s allowed amount rather than the provider’s full list price; however, out-of-network care can result in different balances. Comparing these approaches requires attention to what each model does and does not include and how insurers handle cost-sharing under their terms.

Coding and charge capture are operational factors that can affect bills: services must be documented and coded accurately to be billed and reimbursed. Administrative processes such as preauthorization, clinical justification for expensive diagnostics, and the timing of submissions may influence whether claims are paid promptly or require additional documentation. In some systems, hospitals provide pre-admission cost estimates that may help project likely patient responsibility; these estimates frequently rely on typical case patterns and may change if care deviates from the initial plan. Clear documentation and early insurer communication often improve predictability.

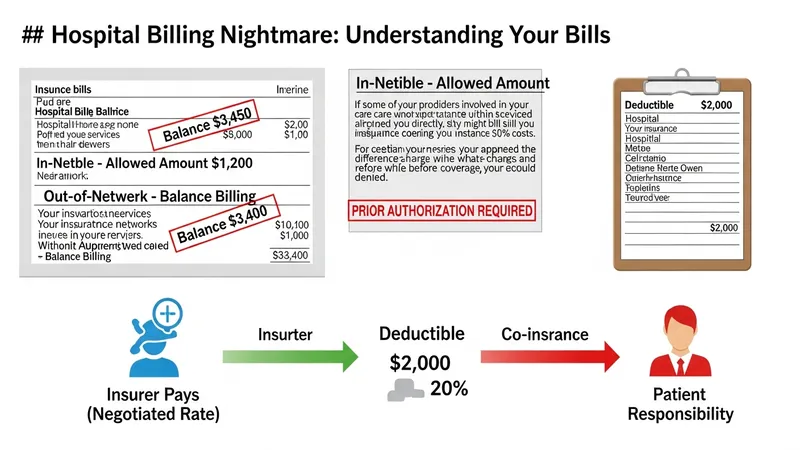

Patient responsibility typically derives from plan provisions: deductibles, co‑payments, co‑insurance percentages, and out-of-pocket maximums. Different insurance designs can change how facility and professional fees are split for the insured individual. For example, a plan with high deductibles may leave the patient liable for significant charges until the deductible is met, whereas comprehensive coverage with limited co-insurance may reduce direct out-of-pocket exposure. It is important to view plan terms in conjunction with the hospital’s billing methods to estimate potential balances rather than assuming a single uniform outcome.

Ancillary categories frequently contribute materially to final invoices. Pharmaceuticals administered during admission, implantable devices, advanced imaging, and laboratory panels can add substantial line items. Some hospitals list these separately, while bundled offerings may group certain standard items and exclude others. Understanding which ancillary items are likely for a given service and whether an insurer typically covers them under the same benefit category can inform cost expectations. In practice, variability in clinical needs means actual invoices may differ from published or estimated totals.

In summary, evaluating costs at privately run hospitals involves parsing fee structures, billing presentation, and insurance interactions. Each component may affect what a patient ultimately pays, and predictable estimates often depend on clear documentation, insurer communication, and awareness of what is included in any quoted price. The next sections examine practical components and considerations in more detail.

Fee-for-service remains a common structure in many private settings; under this model, each discrete service is recorded and billed, which can make invoices detailed but variable. Bundle or package pricing presents an alternative where an episode of care is quoted as a single amount that may include facility use, basic consumables, and a standard length of stay. Contractual arrangements with insurers can introduce third patterns: negotiated schedules, case-based payments, or fixed reimbursements for defined diagnoses. Each structure can influence not only the headline price but also administrative processes such as prior authorization and claims adjudication.

In practice, hospitals may apply blended approaches across service lines. Elective procedures with predictable paths—such as uncomplicated elective surgery—are often candidates for packaged rates, while emergency and complex care typically revert to itemized fee-for-service billing because of variable resource use. Contracted insurer rates frequently modify the effective charge by applying a reduced allowed amount or a percentage-of-charge reimbursement. Patients should therefore be aware that the same procedure can yield differing bills depending on the billing model used by the hospital.

Operational considerations matter: how services are coded, captured in the hospital information system, and transmitted to payers can change the claim result. Common challenges include mismatches between facility and professional billing (separate invoices for surgeon and hospital), omission of bundled components, and delays when additional clinical justification is requested by insurers. Administrative resources such as billing offices and financial counsellors may assist in clarifying invoices, but these processes can add time before final balances are known.

When comparing likely costs across providers, it can help to identify which billing model applies to a given service and what typical exclusions exist. For instance, package rates may explicitly exclude advanced implants or extended ICU stays. Where hospitals publish sample price lists, those figures may reflect average uncomplicated cases and may not account for patient-specific complexity. These distinctions are considerations rather than guarantees, and they encourage closer inquiry into line-item definitions and insurer contractual terms.

Insurance plans commonly influence patient balances through coverage rules such as in-network agreements, deductibles, co-insurance percentages, and prior authorization requirements. When a hospital participates in an insurer’s network under agreed pricing, patients often confront the insurer’s allowed amount and their plan’s cost‑sharing rather than the hospital’s full list charge. Conversely, out-of-network services can lead to higher patient responsibility or balance billing where allowed. Preauthorization protocols may be required for high-cost procedures or specific diagnostics and can affect whether insurers accept claims.

Different plan types—indemnity-style policies, managed care models, or employer-sponsored group plans—may process hospital payments differently. Managed care arrangements often emphasize negotiated rates and may limit access to certain specialists without referrals, while indemnity plans may reimburse according to a schedule or percentage of charges. Supplemental or gap coverage can sometimes cover portions of co-payments or deductibles, but such arrangements are plan-specific. Understanding these distinctions can clarify which portions of a hospital bill an insurer may cover and which are likely patient liabilities.

Claims processing workflows also bear on timing and balance determinations. After a hospital submits a claim, the insurer’s adjudication process can include reviews for medical necessity, coding verification, and coordination of benefits when multiple plans are involved. Denials or requests for additional information can delay payment and produce interim patient statements. In some systems, hospitals will bill patients for unpaid portions while appeals or supplemental documentation are in process, so timelines may be an important practical factor in overall cost experience.

Patients and advisors often consider whether pre-visit communication with insurers can change expected outcomes. Seeking preauthorization where available and obtaining written confirmation of coverage levels for proposed procedures may reduce uncertainty. Similarly, confirming network status of the specific hospital and involved clinicians can alter expected cost-sharing. These steps are informational considerations that may improve predictability but do not guarantee coverage outcomes, which remain subject to plan terms and insurer adjudication practices.

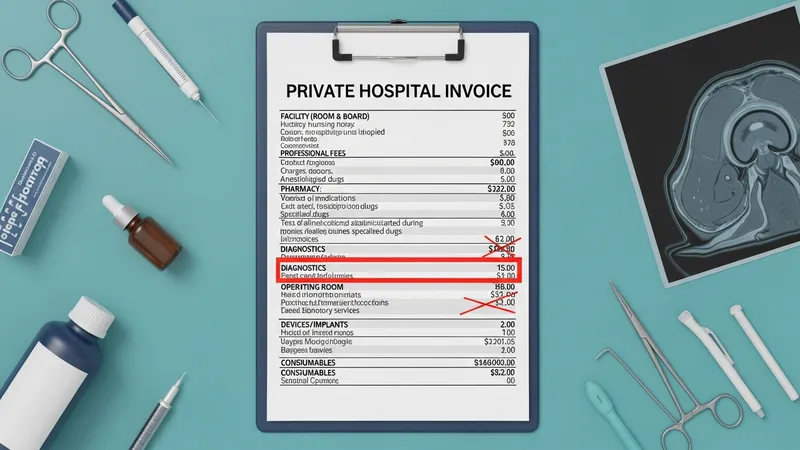

Hospital invoices typically separate charges into categories such as facility (room and board), professional fees, pharmacy, diagnostics, operating room, and consumables or devices. Facility charges often encompass bed use, nursing care, and basic supplies, while professional fees cover clinician services billed independently. Pharmacy and procurements—especially specialty medications or implants—can represent significant additional items. Diagnostic imaging and laboratory testing are commonly listed separately and may be billed at rates that differ from outpatient settings. Understanding these categories helps identify where major cost drivers may arise for a given episode of care.

For surgical admissions, the operating room and implantable device costs frequently influence overall totals. Some hospitals include standard implants or prostheses in packaged prices, while others list them separately; similarly, advanced imaging or interventional radiology procedures may be excluded from flat packages and thus produce extra line items. In medical admissions, prolonged stays, specialty consultations, and high-cost medications can change the composition of the bill. These patterns are typical rather than universal and may vary by clinical complexity and local practice norms.

Billing transparency practices can differ: some hospitals produce itemized bills showing unit costs and service dates, while others provide summarized statements with limited detail. Itemized invoices may facilitate insurer claims and patient review but can also be more complex to parse. Patients who review line items often look for duplicate charges, mismatched dates, or items that should have been bundled. Where available, hospital financial offices or independent billing advocates may explain line-item meanings; such explanations are informational and intended to clarify rather than to alter clinical decisions.

When estimating potential costs, clinicians’ choices and patient-specific factors such as comorbidities, age, and procedure complexity commonly influence resource use. For example, an uncomplicated elective admission typically involves fewer diagnostics and a shorter length of stay than a complex or emergency admission. These clinical variations translate into differences in billing categories and totals. Recognizing that service composition, not only headline procedure rates, shapes invoices is a practical consideration when evaluating private hospital costs.

Billing cycles commonly start with an initial admission or discharge statement, followed by insurer adjudication and eventual patient billing for any remaining balance. Timing can be affected by claim submission schedules, insurer processing windows, and appeals if coverage is disputed. Hospitals may offer itemized statements and access to billing staff who can clarify codes and dates; these services are informational and may assist in understanding charges. Some providers may provide estimates before elective care, though such estimates may change if clinical circumstances evolve during treatment.

Patient-level factors that typically influence final expenses include plan details (deductible and co-insurance), whether clinicians are in-network, and clinical complexity requiring intensive resources. Pre-existing conditions or unexpected complications can extend lengths of stay and increase use of high-cost services such as critical care or advanced therapeutics. Coordination of benefits when multiple insurers are present may change how claims are processed and apportioned. Viewing these items as variables rather than certainties can help frame expectations when comparing providers or planning care.

Administrative practices also affect patient experience: clear preauthorization processes, timely submission of claims, and accurate coding reduce the likelihood of denials and subsequent patient statements. Where disputes arise, appeals procedures and supplementary documentation may resolve issues but can extend the timeline before final balances are confirmed. Financial counselling services in some hospitals may present payment plan options or explain insurer responses; these are procedural choices intended to manage cash flows and documentation rather than to affect clinical choices.

Finally, broader considerations include regulatory and market contexts that shape provider pricing and insurer behavior. Local competition, regulatory reporting requirements, and standard contractual practices among hospitals and insurers can influence the availability of published rates and the prevalence of packaged offerings. These systemic factors often determine how transparent costs are in practice and should be viewed as background considerations when assessing individual hospital bills and insurance interactions.